This is the fourth in a series of features written by Keith Mallinson (WiseHarbor) for IP Finance. In this piece, Keith contrasts different structures for establishing the price paid for use of IP in the context of essential standards and concludes that, while voluntary patent pools have sometimes had beneficial results, pools should never be imposed because their imposition would eliminate significant competition from originates from outside pools; mandatory pools with royalty caps would both be anticompetitive and impede competition. "Fixing IP Prices with Royalty Rate Caps and Patent Pools

Whereas voluntary patent pooling is common in licensing standards-essential IP for digital audio and video, attempts to impose pooling on licensing complex products, which include multiple standards and many more patents, are ill-suited and potentially anticompetitive. Some companies may voluntarily form patent pools for any particular standard, but mandatory patent pools seeking to limit licensing fees would distort competition by favouring downstream licensees at the expense of upstream licensors who depend on licensing fees to fund their R&D. IP owners, including vertically-integrated companies which combine downstream product businesses with upstream technology licensing, generally prefer bilateral agreements for IP-rich products such as mobile phones. Unlike patent pools, bilateral licenses most frequently include technologies for several standards and other IP, whereas each pool may only include essential patents for just one standard. Technology and market developments are best when competition facilitates various business models and licensing practices. And that also benefits consumers.

Licensing Cartels: From Monopoly to Monopsony

There is a long history of patent pools being used to monopolise markets, excluding competitors and controlling prices in several cases.

Adam Smith and others typically depict price fixing as conspiracy against the public to raise prices. However, there is another way to fix prices: collusion to reduce prices paid to suppliers. Forcing technology input prices lower would starve upstream technology developers of the profit margins required to sustain employment, reinvestment and their output in technology development. Ultimately this would be to the detriment of consumers who benefit from rapid and dynamic innovation in ICT and elsewhere. Reduced licensing fees do not guarantee lower consumer prices. With concentration in supply downstream, manufacturers may take the savings in profits.

Nevertheless, calls for mandatory or strongly encouraged participation in ICT patent pools are an increasing trend—typically from downstream licensees and their customers—with the self-serving objectives of limiting their input costs. Some well-intentioned policy makers also mistakenly regard patent pools as a panacea for supposed problems with complex patent landscapes and patent quality.

In-licensing requirements highest among those with most IP

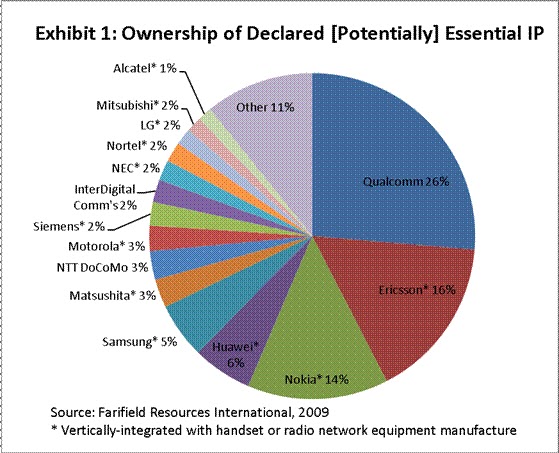

Manufacturers with little or no IP and vertically-integrated companies with extensive IP are all dependent on in-licensing for most IP required in today’s ICT products, such as mobile phones. Technology ecosystems are complex webs including those who create new technologies and those who implement them in products. No handset manufacturer has declared more than a small minority of the IP required to implement 3G cellular. Technologies developed by scores of different companies are shared in implementation by hundreds of downstream manufacturers.

Exhibit 1, based on data from a 2009 study funded by Nokia, shows that leading implementers Ericsson, in radio network equipment, and Nokia, in handsets, declared IP ownership amounting to 16% and 14% respectively of the total for 3GPP mobile communications standards with WCDMA. Leading technology and chipset provider Qualcomm declared 26% ownership. (Many have claimed the study methodology is flawed. The input data is used here to demonstrate the well accepted fact that many companies have patents related to these standards).

![]()

With the need to in-license most essential IP, it is no surprise—with self-interest rather than altruism— manufacturers and their downstream customers (mobile operators who in many cases subsidise handset prices to consumers) have striven to limit aggregate licensing fees. A common proposal from several mobile operators is to limit aggregate essential-IP charges by establishing an LTE patent pool with that specific objective. For example, would-be pool administrators Via Licensing and SISVEL have promoted themselves and pooling over the last two years by scaremongering about the threat of so-called royalty stacking. In one presentation, Sisvel nonsensically projected WCDMA royalties at twice average wholesale prices. I analysed aggregate royalty levels in my last posting here and concluded that aggregate fees are modest and merited by those that invest significantly in risky R&D.

The European Commission

DG Comp’s Draft Horizontal guidelines recognise that vertically integrated companies that both develop technology and sell products "have mixed incentives". Companies with a significant share of a downstream manufacturing business generally face higher costs in licensing fees for the IP they do not own than they can generate in licensing fees from the IP they do own. This explains the 2008 attempt by Alcatel-Lucent, Ericsson, NEC, NextWave Wireless, Nokia, Nokia Siemens Networks and Sony Ericsson to cap below 10% aggregate royalties for handsets implementing the 3G/4G LTE standard, as

described in my previous IP Finance posting.

Proposed caps are for aggregate maximum rates to be paid for all standards-essential patents owned by all patent holders. However, in practice, net royalty payments are zero or are minimized among vertically-integrated companies who cross-licence, with or without a cap – so a proposed cap would have little or no impact on licensing costs among such companies. The latter would greatly benefit from any reduction in upstream licensors’ fees—payable by all licensees—whereas, any squeeze on their own charges would only be significant in the minority of the market where they are not cross-licensing to minimise or eliminate net payments. A manufacturer’s IP fee income is generally small compared to its product revenues.

IP licensing, before and after imposition of an aggregate royalty cap, is depicted in Exhibits 2a and 2b respectively. In this simplified yet representative model, 75% product market share (applicable for handsets sold in 2010) is supplied by vertically-integrated manufacturers who minimise royalty charges among themselves. Product markets are predominantly supplied by those who hold significant essential IP—even excluding Apple, RIM and HTC who had no essential IP until after 2006, according to the source used in Exhibit 1. Manufacturers with the largest patent holdings also tend to have the largest shares of the downstream markets for which they need to license-in most IP. Smaller manufacturers with significant IP have negotiating leverage over larger players because the latter need licensing for relatively large shares and revenues in product markets. The remaining manufacturers, without IP, who account for the other 25% of market share, instead pay fees for all IP licensing required. Upstream licensors charge fees to all manufacturers downstream to fund R&D investments. Also consistently with declared IP ownership in Exhibit 1’s source, it is assumed that manufacturers without IP to trade make one third of their out-payments to upstream licensors and the remainder to vertically-integrated players. As an example, the royalty cap modelled is an arbitrary reduction of one third to the aggregate royalty rate (as a percentage of handset prices). Total licensing fees paid, received, and reduced are proportional to the areas of the various coloured blocks on the two diagrams.

![]()

The result is that aggregate royalty rate caps save money for all downstream manufacturers at the expense of upstream licensors. Downstream manufacturers with no IP to trade save most significantly. In this model, vertically-integrated companies lose some revenue, but save significantly more in reduced expenses. For every dollar of licensing revenues they lose through any capping, they save $1.50 in licensing out-payments to upstream licensors. Licensing fees to upstream licensors from all manufacturers fall in the same proportion.

Fish too big for the pool

Several voluntary patent pools established in the last decade or so have been quite successful. They have attracted many firms to join as licensees. This collective out-licensing is efficient because the pool administrator can serve as a distribution channel for many licensors and as a one-stop-shop, subject to the pool standard’s limited scope and IP contributed, for licensees. Research reveals that recent pools for audio and video codec standards-essential patents have attracted, in most cases, the majority of the standards-essential patents for those standards, including MPEG-4 with 34% of firms that have applicable patents contributing 89% of the required patents. This research also concludes that while a number of vertically-integrated companies who manufacture products implementing the standards are most inclined to join, many vertically-integrated and upstream essential-IP owners decide to stay out. Some IP owners find they can derive more value from bilateral licensing and cross licensing, or that pools do not provide sufficient freedom to pursue and defend their downstream businesses. Specific concerns include:

- The difficulty of determining how to share pool profits with thousands of patents, uncertainties around essentiality and the relative values among patents;

- Differing business models with upstream licensors and vertically-integrated manufacturers holding major proportions of essential IP;

- Asymmetries in patent ownership among these manufacturers and versus upstream licensors;

- The need to license devices for multiple standards with 2G, 3G, 4G, video, audio and for other technologies outside of the standards; meaning that bilateral deals, which can encompass all of a company’s IP, are always going to be necessary, and are more flexible;

- The need to resolve significant patent litigation with fierce competition between vertically-integrated manufacturers and other end-user product manufacturers without standards-essential IP.

This is mostly achieved through bilateral settlements which likely would be extremely difficult if the companies had agreed to, or been forced into, patent pools.Pooling IP would surrender control of this most strategic asset for several major players; and mandatory pooling would expropriate this valuable private property. For example, it could have limited Nokia’s ability to sue Apple for significant licensing fees in 2009, based upon Nokia’s standards-essential WCDMA patents, and then expediently agree to settle for cash in face of counter-suits and deteriorating Nokia finances with a profit warning most recently. In contrast, the 3G Licensing pool has never sued for patent infringement. While announcing settlement of patent infringement litigation with Apple, Nokia’s CEO, Stephen Elop, stated that Nokia’s cumulative R&D investment during the past two decades was Euro 43 billion ($60 billion). This is largely justified by sales of its own products and by minimising aggregate royalty out-payments, stated to be less than 3% gross to 2007, through bilateral licensing. Fees to be received in the cross-licensing settlement with Apple–now with revenue share close to market leading levels of Nokia and Samsung–were not disclosed. Whereas Google does not manufacture anything, HTC and Samsung are being sued by Apple for infringement, of patents that are not essential to the mobile standards, by their smartphone devices employing Google’s Android operating system. Google made a stalking-horse bid of $900 million for a portfolio of 6,000 patents, including essential IP, from bankrupt Nortel. The patents would have had great defensive value to Google, who makes its money from advertising in search on PCs and phones using its software and services, but has a limited patent portfolio. However, a consortium of Apple, Microsoft, Sony, Research In Motion, Ericsson, and EMC obtained Nortel’s patents for $4.5 billion. The consortium rules are unknown publicly, but presumably the members will be able to use the portfolio defensively in bilateral license negotiations and litigation settlement discussions.

Absent (misguided) regulatory fiat, there is no reason why an LTE pool would become any more significant than the unsubstantial and struggling WCDMA pool. Attempts in the early 2000s by the 3G Patent Platform Partnership (set up by some telecom companies as a voluntary pooling arrangement) to regulate 3G IP fees with collective licensing and a “Maximum Cumulative Royalty Rate” of 5% were unsuccessful. The WCDMA patent pool includes mainly mobile operators and Japanese manufacturers. It covers only around 10% of patents declared by the patent holders to be WCDMA standards-essential. Multimode, multi-media devices (e.g., smartphones, 3G tablets) are incorporating increasing numbers of cellular and other standards. Proposed LTE patent pools have also made little progress over the last couple of years for all of the same difficulties faced by the 3G patent pools.

No panacea

Manufacturers, including the vertically integrated with significant IP, have self-serving incentives to cap aggregate royalties. Caps would reduce downstream product licensing costs significantly more than they would reduce licensing revenues for the latter. However, these companies tend not to favour patent pools for other reasons. Unfortunately, the significant shortcomings are not recognised by many policy makers who mistakenly see patent pools as a panacea to solve supposed problems with complex patent landscapes. Voluntary patent pools have been beneficial in some cases, but patent pools should never be imposed because this would eliminate significant competition that comes from outside of pools. Mandatory pools with royalty rate caps would be anti-competitive and impede innovation".